Editor’s note: This brief is part of the Vermont Agriculture & Food System Plan 2021-2030 submitted to the legislature in January 2021. To read the full plan, please go to

Lead Author: Erin Buckwalter, NOFA-VT

Contributing Authors: Jennie Porter, NOFA-VT; Jean Hamilton, Consultant; Alissa Matthews, VAAFM;

Andy Jones, Intervale Community Farm; Sherry Maher, Brattleboro Winter Farmers Market.

What’s At Stake?

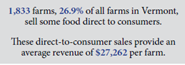

Over a quarter of Vermont farms (1,833) sell directly to consumers through farmers markets, Community Supported Agriculture (CSA), and other “direct market” channels. Direct markets are critical because they allow producers to capture more income for each product sold (compared to wholesale), require low up-front investment, give producers more autonomy over the products they sell, and foster customer relationships through experiential marketing (an increasingly

important tactic across all industries). The trends towards consolidation and downward price pressure in wholesale markets favor larger producers and create challenges for many small to medium-scale producers, accentuating the importance of strengthening direct markets as the foundation of a working landscape of diverse farms at all scales.

Current Conditions

Since their revival in the 1970s, Vermont’s direct markets have been a critical market channel for producers and must continue to be a priority for focused market and business development. In addition,direct markets serve as a common entry point for shoppers who may be new to purchasing local food. In 2017, Vermont direct market sales totaled $49.9 million. Farms often rely on direct markets as part of a mix of market outlets critical to their business viability. The USDA’s Economic Research Service found, “farmers who market goods directly to consumer are more likely to remain in business than those who market only through traditional channels” and that, for beginning farms, having direct markets as part of the business increased the chances of business survival. Through the 1990s to early 2010s, a boom in direct markets, buoyed by the burgeoning “local food movement,” coincided with growth in diversified farms across the state. This success brought competition from large retailers and corporations claiming “local” as a marketing term, sometimes misleadingly, leading to concerns about the viability of direct markets.

Competition also increased innovation from direct market farms, from on-farm events to responding to consumer demand with more flexible CSA models (see Agritourism brief).

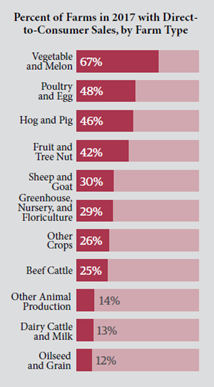

Results from the 2017 USDA Census of Agriculture show that direct sales are increasingly important to the bottom line for Vermont farms, with average sales per farm through direct market channels more than double those in 2012. Consumers in Vermont are spending more money in direct markets channels as well, with sales increasing over 82% from $27.4 million in 2012 to $49.9 million in 2017. Direct-to-consumer sales in Vermont made up over 24% of total local food and beverage purchases in 2017 and 3.3% of overall food and beverage purchases.

Various organizations provide marketing assistance to producers, conduct statewide consumer campaigns about the benefits of direct markets, foster collaborative marketing between direct marketing businesses, and work to connect shoppers and visitors to Vermont producers. These promotion and technical assistance programs represent a solid foundation to expand upon.

Bottlenecks & Gaps

• Increased consumer demand for local food has resulted in distributors and retailers with vast

marketing resources claiming products are “local,” even if their claims are not in line with customer

expectations. This puts downward price pressures on farmers and challenges their viability.

• Direct market farmers are now competing against large companies able to capture customers looking for convenience through new marketing models such as online ordering, meal kits, and home delivery.

• Direct market farmers often lack the marketing skills, technology, broadband access, and funding necessary to reach modern consumers in this competitive environment.

• Many farmers markets lack resources to support professional staff, which impacts their capacity

for marketing, managing vendors, securing stable locations, handling legal issues, providing good

consumer experiences, etc.

Opportunities

• Consumer trends show people are looking for a relational form of food purchasing. Vermont can

capitalize on these trends with increased marketing for, and storytelling about, direct markets (see Consumer Demand brief).

• Collaborative marketing is already happening at various levels (statewide, regional, groups of farmers) and can be built upon to support individual producers and farmers markets unable to compete with the marketing savvy of large companies.

• Online technology exists that can enable local producers to grow their web presence and reach a

potential new customer base.

• Direct markets that participate in public health and/or food access programs such as SNAP/3SquaresVT, EBT incentive programs, etc., ensure that all Vermonters can access local food from direct markets and producers can receive income from federal food assistance programs (see Food Access and Farm Viability brief).

Recommendations

• Provide $500,000 annually in state funding for a collaborative, statewide marketing and consumer messaging campaign to focus on the unique attributes and values that direct markets offer, building affinity for shoppers to support direct markets.

• Provide annual funding for two FTE positions: one to provide centralized resources and marketing support to Vermont’s direct market producers, and one for the Vermont Farmers Market Association to provide centralized resources and marketing support to its members. Estimated cost: $150,000 for two FTEs.

• Assess what resources would be needed in order to purchase/dedicate public land for eight “flagship” farmers markets across the state through land trusts, Vermont State Parks, or some other body that can help institutionalize market locations.

• To increase their sustainability and impact, provide funding to include farmers markets in business assistance programs like the Vermont Farm and Forest Viability program. Funding would include stipends for the markets to dedicate a staff person to participate in the program. Estimated cost: $3,000 per market.

• To expand direct markets’ ability to support public health/food access, create a state funding source devoted to perpetuating NOFA-VT’s statewide direct market EBT doubling programs. Estimated cost: $43,000 annually to support equipment and fees for 45 farmers markets and 20 farms.

• Develop peer-to-peer training and outreach to share success stories of producers that have been experimenting with online farm stands and customizable CSA models.